DENVER — With a warmup on the way after several days of subzero temps, many Coloradans may soon hear the dreaded "drip, drip" as pipes that froze during the cold burst.

We asked Carole Walker, executive director of the Rocky Mountain Insurance Information Association, what homeowners should do if their pipes burst, causing flooding inside their homes.

While they don't typically cover flooding that comes from outside your home, most insurance policies do cover water damage caused by frozen pipes.

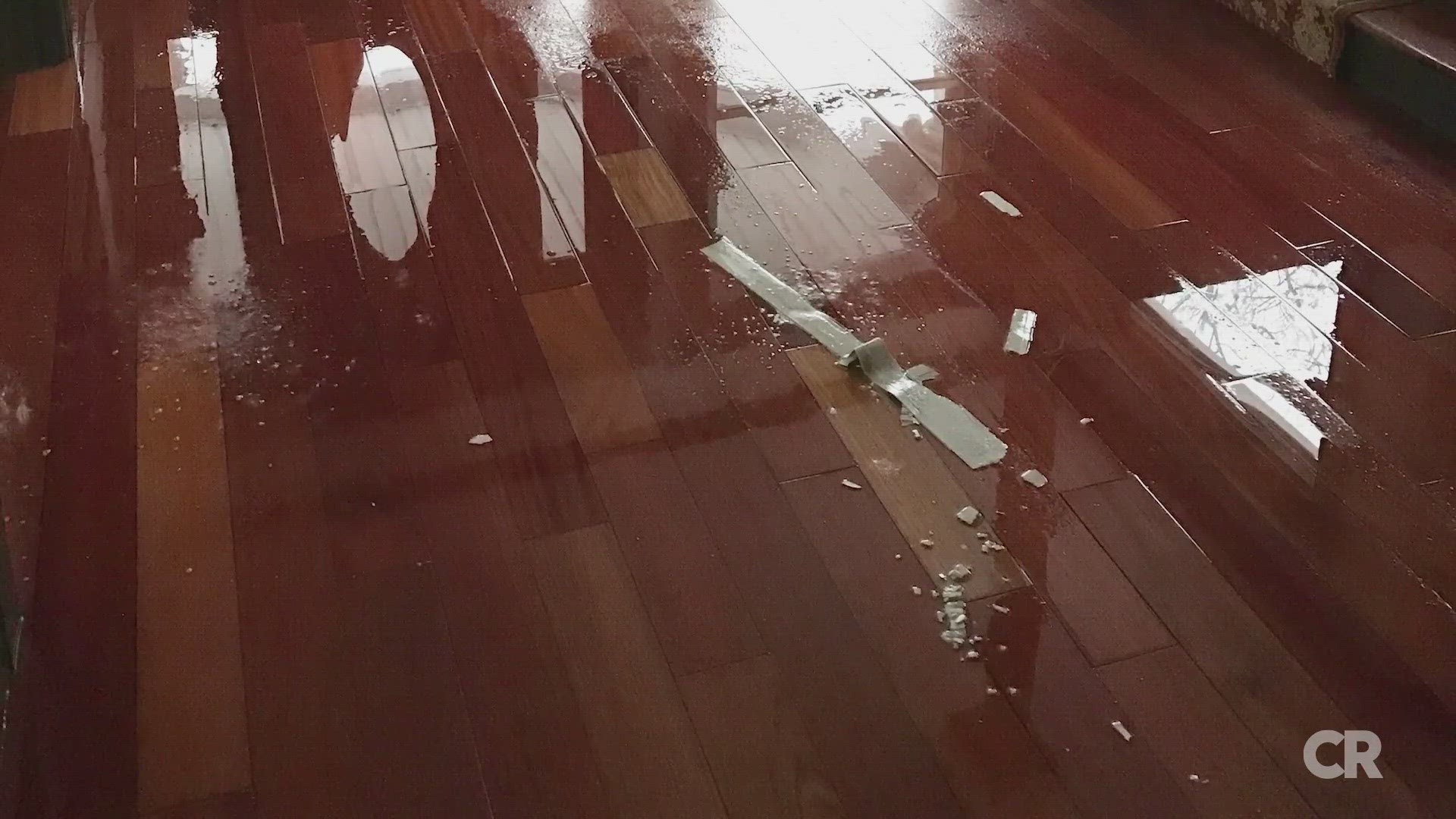

Step 1: Shut off your water and clean up as much as possible

“If it does burst, mop it up, turn off that emergency water valve, and then get in touch with a professional to get in there,” Walker said.

Everyone in your home should know where the emergency water shutoff is in your home. Our partners at Consumer Reports say the shutoff is often located on the wall of the basement along the front of your home along a vertical copper or PVC pipe.

Walker said water from pipes that burst can seep into odd places and cause a mold issue, so you should try to mop up as much of the water as you can.

“Make some temporary repairs, and then hang on to those receipts from those repairs,” she said. “Because they will be reimbursed when you go to file a claim.”

Step 2: Contact your insurance company

As you work to handle the problem, Walker said it is important to document as much of it as you can.

“Make sure that you're taking photographs of everything, get in touch with your insurance professional immediately and get that claims process started,” he said.

Your insurance agent can also help in the next step of the process – finding a legitimate contractor to do any work you need to have done.

Step 3: Find a reputable contractor

“Picking the right contractor is so important because unfortunately, any time we have the deep freeze like this, it's also going to attract those scam artists,” Walker said.

When picking a contractor, Walker recommends seeking references.

“You want to make sure that you're checking out their references. Word of mouth is still the best bet. You can also check them out through the BBB, the Secretary of State's site,” she said. “Any good contractor is going to have a trail online.”

Walker said one red flag to watch out for is a contractor who wants full payment before any work is done.

“If you have insurance, most reputable contractors will understand that you're going to get a certain amount from your insurance company,” she said. “And when they complete the work, that will be a final payout.”

What if I’m a renter?

Walker said if you’re renting a home or apartment and a pipe bursts, your landlord’s insurance will likely be on the hook for any necessary repairs. But a renters insurance policy would cover any personal items you have to replace that were damaged by the flood.

“Any type of water damage or winter weather damage, you have risk of destroying all of your things -- everything from your expensive computer and appliances. Anything that you own, you should have a renters policy on that will cover you to repair and replace those items covered under a renter's insurance policy,” Walker said.

Have a tip for Consumer Investigator Steve Staeger? Fill out this form to send a tip to Steve On Your Side.

SUGGESTED VIDEOS: Steve on Your Side